Second Charge Term Mortgages

Unlock Extra Funds Without Changing Your Main Mortgage

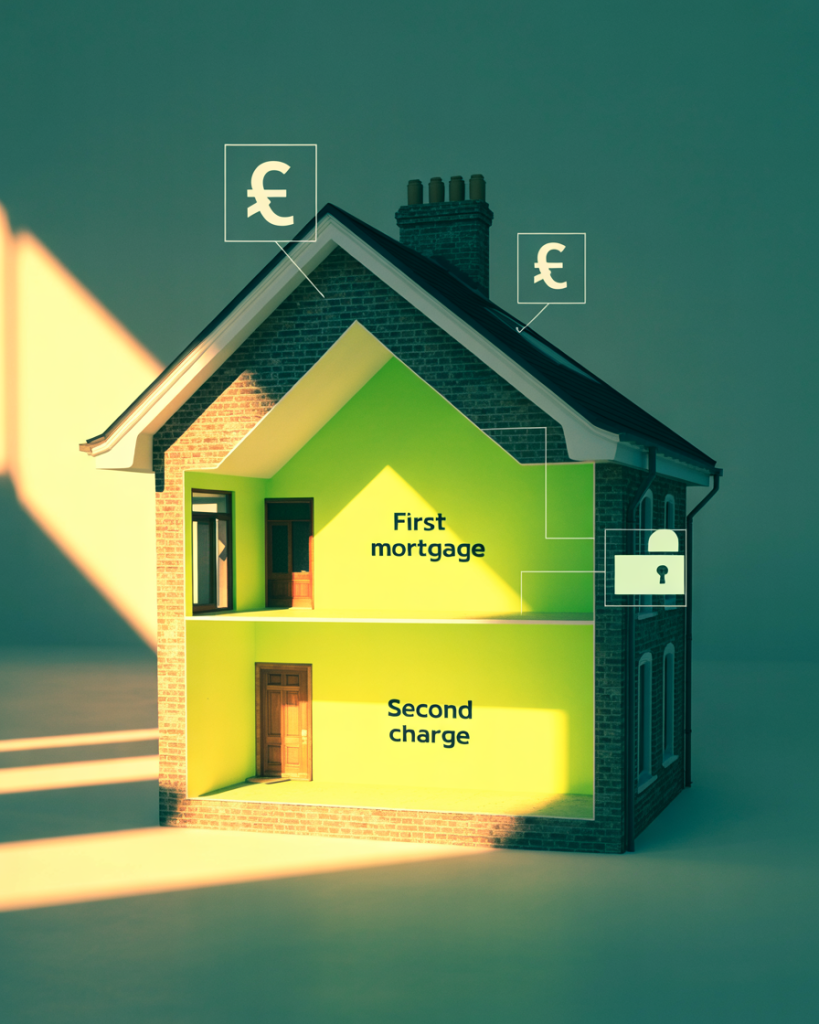

Unlock Equity Without Touching Your First Mortgage

Need to raise funds without disturbing your current mortgage deal? A second charge term mortgage lets you borrow against your property while keeping your first mortgage in place. This can be a smart choice if you have a great rate you want to keep or want to avoid early repayment charges.

At Bridging Finance Broker, we help homeowners and landlords arrange second charge term mortgages designed for long-term plans, whether that is home improvements, debt consolidation, or business growth.

What Is a Second Charge Term Mortgage?

A second charge mortgage, also called a secured loan, is a facility that sits behind your existing mortgage. Rather than remortgaging or taking out a personal loan, you can release equity from your property to raise funds.

Term-based: Usually repaid over 3 to 30 years

Monthly repayments: Fixed or variable interest options available

Flexible use: Ideal for home improvements, debt consolidation, business investment, or personal spending

It can be a smart alternative when remortgaging is costly, complicated, or not the right fit for your circumstances.

When Does a Second Charge Make Sense?

You're on a low rate mortgage and don’t want to remortgage

You have early repayment charges on your first mortgage

Your income or credit has changed and a remortgage won’t work

You need funds quickly but want a structured repayment over years

What Can You Use It For?

Home improvements such as extensions, new kitchens, or loft conversions

Consolidating multiple high-interest debts into one affordable payment

Paying school fees or providing financial support for family

Funding business growth, new projects, or improving cash flow

Purchasing an additional property or investing in opportunities

Who It's For

Homeowners with equity in their property

Buy to let landlords raising funds

Self employed borrowers with complex income

Clients who cannot or prefer not to remortgage

We can arrange both regulated and unregulated second charge mortgages, depending on whether the property is or will be your home.

Key Features and Lender Criteria

Loan size: £10,000 to £2 million+

Term: 3 to 30 years

LTV: Up to 95% combined (first and second charges)

Rates: From 6% p.a. (fixed or variable)

Repayment: Monthly instalments (capital and interest)

Credit profile: Options available for applicants with adverse credit

Some lenders may also offer interest only or alternative repayment structures.

The Application Process

Initial consultation

We understand your goals, income, and property value

Product match

We search the market and recommend tailored lenders

Valuation & paperwork

We help you gather docs and book a valuation

Lender review

Underwriting checks and offer issued

Funds Released

Direct to you or to creditors (in consolidation cases)

Clear Communication

No jargon, no confusion, no chasing we keep you updated every step

Use Our Mortgage Calculator

Curious what your repayments might look like? Use our calculator to estimate monthly costs based on loan size, term, and rate.

Frequently asked questions

Everything you need to know about the bridging finance broker

Is a second charge mortgage right for me?

If you’ve got equity and want to keep your main mortgage intact, it’s a great solution.

Can I apply with bad credit?

Yes, some lenders specialise in adverse credit. We’ll assess your options.

Can I use a second charge on a buy-to-let property?

Yes, landlords often use second charges to fund portfolio expansion or refurbishments.

Do I need my first lender’s permission?

Yes, but we’ll manage the process and work with lenders familiar with second charges.

Access the Equity You’ve Built Without Starting Over

We help you unlock capital while protecting your current mortgage rate giving you flexibility, speed, and structure.